wildpixel/iStock via Getty Images

Introduction

No matter where an investor tunes in today, a single word dominates the market commentary: Recession. The word recession, often closely followed by a discussion of “stagflation” and “soft landing”, is on everyone’s lips. And because we haven’t experienced a “normal” recession in well over a decade (2020 was too unusual to count in my book), many investors have not experienced what it’s like to invest through an extended recession. In this article, I’m going to share my views on both recessions, and bear markets, in hopes that newer investors can get a perspective from someone who has invested through the 2000-2002 bear market, as well as the recession in 2008/9 and the crash of 2020.

My approach to this process is rooted in sharing what I have been doing to prepare for a bear market and recession. I take this approach for two key reasons. The first is that too often there is a big disconnect between what financial writers say, and what they are actually doing. One of my goals is to close that gap by sharing not only what I have been thinking, but also what I have been doing. The second reason is that I want to give investors specific examples from the real world, not so that they can follow the examples themselves necessarily, but so they can see the underlying principles at work, and perhaps consider how those principles might, or might not, apply to their specific situation. So, as you read this article, I would encourage you to be mindful more of those underlying principles than the specific stocks I might have bought or sold.

Recession vs Bear Market Distinction

The first thing investors should consider when it comes to recessions is the distinction between a recession and a bear market. A recession has to do with the real economy, and a bear market has to do with the aggregate price of stocks. There is no perfect definition of either term, but the general guidelines for a recession are two consecutive quarters of negative GDP. And for a bear market, a price decline from the peak of -20% or more for a major index like the S&P 500.

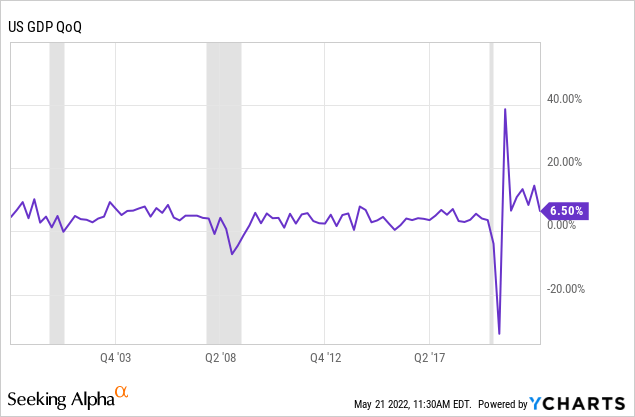

We can see in the chart above of QoQ GDP since 1999, usually, recessions occur when QoQ GDP is negative for consecutive quarters, as in 2008 and 2020. Right now it’s at 6.50% (though falling pretty rapidly). But in the 2002 recession, GDP never quite went negative for two quarters in a row in the chart above, yet economists still called it a recession. Still, during that 2002 time period which is generally considered a mild recession, the stock market was crushed:

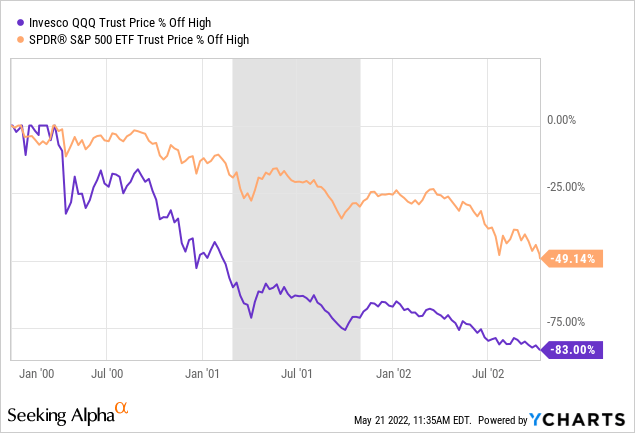

From 2000 to 2002, Invesco’s (QQQ) ETF and the S&P 500 were down -83% and -50% off their highs during this time. This is very important for investors today to understand for two reasons. The first is that 2002 was a fairly mild recession, yet the stock markets dropped a lot. So there can be a mild recession that coincides with devesting losses in the stock market. In fact, I think it’s fair to say that the market decline in 2000 and 2001 was a primary contributor to the recession itself, rather than an economic contraction occurring first, and then having the market react to that, which is closer to what happened in 2008. The second reason this is important to understand is economic leading indicators were not very useful at predicting the timing or severity of the 2000-2002 market decline. If you were in the QQQ or similar stocks at the time, and you waited for leading economic indicators to tell you when to sell your stock positions, you would have been down about -60% before any clear sell signal came from the economy.

So, the first question we have to ask ourselves is whether we are in a situation where the market leads the economy down or the economy leads the market down?

This was the same question we had to ask ourselves in February of 2020 as well when coronavirus came on the scene. On February 28th, 2020, when I decided to go into what I termed “recession mode” at the time, I decided that the unusual nature of the coronavirus meant that leading economic indicators were not useful, and I decided to rely strictly on a technical indicator. Here is what I had to say in an SA blog I shared the next day on February 29th titled “Recession Mode Has Arrived” where I explain my reasoning for the recession call even though the Leading Economic Indicators still looked okay:

It was the use of the LEI where the market kind of threw a wrench into the works again. Technically speaking, the LEI had not quite met the conditions I originally set out in my strategy, but it was close to meeting those conditions. However, I felt that the coronavirus created a special situation where we can basically look at the news and tell with reasonably high probability that the economy, which was already getting weaker, is going to be negatively impacted. (Or, at least I made the judgment that there is a very high probability of that happening.) Essentially, I felt the purpose of using the LEI was to get ahead of coming economic weakness, but because of the nature of the coronavirus, I judged the news, in this case, was leading the leading numbers of the LEI, and I called this second [recession] condition met.

I’ve had several commenters on my warning articles this year point out that leading economic indicators are still strong, and therefore we are nowhere near a recession. And that might very well be true. But in both the year 2000 and in February of 2020, the leading economic indicators were not useful at preserving investors’ capital. This is why the distinction between a bear market and a recession is so very important. We could theoretically

find a way to avoid a recession altogether and stock investors could still be crushed.

For that reason, preparing for a recession, and preparing for a bear market require different actions. And so I’m going to take the recession question first, and then follow that up with the question of what investors should consider about a bear market.

Are We Heading For A Recession in 2022?

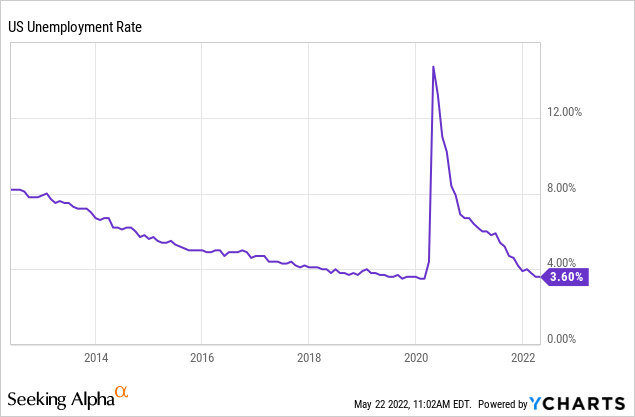

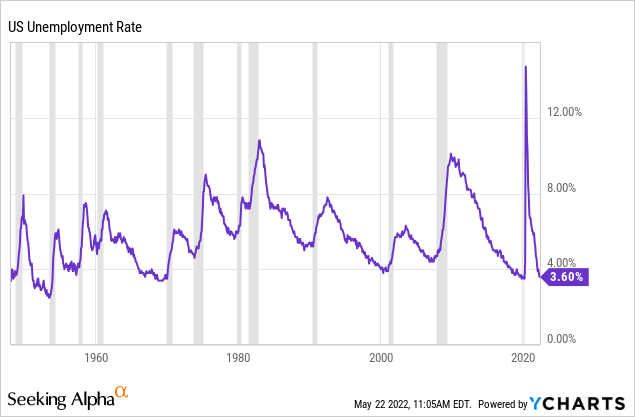

I think we are certain to have an economic slowdown in the second half of 2022, but the odds are much lower of an official recession. The reason I think this is because unemployment is still very low, there are parts of the economy that have substantial cash to spend, and credit is still widely available.

We are basically at historical lows when it comes to the unemployment rate, and it usually takes some time for this to adjust before a recession starts.

Usually, it takes a little time after the unemployment rate falls to these levels before we have a recession. Again, the year 2000 is a good corollary, as is the late 1960s. In order to have a recession in 2022, a steep decline in GDP would have to basically happen next quarter. Given that many Americans already have vacation and holiday travel plans made, and that they will borrow if they have to in order to carry out that pent up demand, while I think we could certainly see a decline in retail and manufacturing and some other areas of the economy, much of that slack will probably be picked up by the service sector. Also, with companies having just gone through a very tight labor market, that, for demographic reasons (like boomers retiring) and pandemic reasons (over a million people dying sooner than normal in the US), I think most businesses will be slow to reduce their staff, knowing how difficult it might be to find replacements in the future. It probably won’t be until Q1 of 2023 after the travel and holiday seasons that most businesses really sit down and assess any future “right-sizing”.

Additionally, wealthier Americans actually still have cash to spend. So, there are going to be parts of the economy that cater to older, wealthier people, that continue to do reasonably well over the rest of the course of this year. These well-off people aren’t going to change their plans just because their stock holdings are down … at least not this year.

So, the good news is that an economic recession in 2022 is likely a low probability event. This means you have some time to prepare for a recession in 2023 which I think actually has a very high probability of occurring, perhaps as soon as Q1 2023.

What Happens During A Recession?

The most important things you need to understand about a recession, are that credit is the same thing as money in the economy, and credit becomes both scarce and expensive during a recession. Ray Dalio does a fantastic job of explaining how these debt cycles that cause recessions work in this video. The key things to understand are that credit becomes more expensive (as the Federal Reserve raises interest rates), people and businesses who are overextended on credit default, or lower their spending in order to cover the higher interest rate payments, which lowers demand in the economy, and because the risk of defaults rise, lenders are less willing to lend at all. This pattern feeds on itself and it leads to an economic contraction we call a recession.

So, because one person or business’s credit is another person or business’s income, when credit contracts so do incomes, falling incomes lead to defaults or less spending, and that leads to less available credit and more expensive credit, which continues the downward spiral until there is an intervention by the Federal Reserve to supply additional credit or lower rates, or, an intervention by the government to supply incomes to people via tax cuts or helicopter money.

That’s the short version of what happens during a recession. Right now both the government, via the ending of stimulus, and the Federal Reserve via the raising of interest rates, are implementing policies that usually cause recessions. And they likely will this time as well if the policies do not reverse soon. However, it takes time for these things to work their way through the economy, and we are just now starting to see the very beginning of the effects. The full effect probably won’t come until later this year or in 2023.

What should investors consider about a recession?

This is where the distinction between a bear market and a recession is important. A recession involves your personal finances more than your stock holdings, while a bear market involves your stock holdings more than it does your personal finances. Preparing for a recession involves things like reducing personal debt (because credit dries up and becomes expensive), building an emergency fund (again, credit dries up so in an emergency credit might not be available at reasonable rates), improving the likelihood of your job security (because jobs are often cut), and, perhaps holding off making major purchases that might have lower prices over the next 12 to 24 months (because prices for goods often fall during a recession).

Each person’s situation is different, so these topics are hard to write about to a broad audience, but here are some of the things I’ve been doing as a middle-class, middle-aged guy, living in the Midwest with a family of four.

- I make sure to pay my credit cards off every single month. This should probably always be the case, but it’s even more important before we go into a recession.

- I pay my mortgage four months in advance. This is a way to always have a cushion in case something comes up like a job loss or medical emergency. It provides a cushion if income is disrupted for any reason.

- I don’t have a car payment, and even though I’m ready for a new car, I am holding off on that purchase (as well as holding off the purchase of a potential RV) because prices are too high and are likely to come down if we have a recession. (I think this is true of the housing market as well.)

- I have about three months’ worth of easily accessible cash, and another 6-9 months of cash that might take a little longer access, but that is available if needed.

- I’m not doing any major voluntary home improvements when input prices are this high.

- I took my more expensive family vacations in 2021 (Hawaii, Yosemite/California, and Arizona) when fewer people were traveling, and this year I will take a relatively cheap vacation closer to home while flights, lodging, and gasoline are very expensive.

- I never use margin or leverage to invest, anyway, but now would be a particularly dangerous time to do so.

I’ll add that it’s probably not a great time to leave a stable job and start a new business

for most people. I did that in early 2008, and I even had a backup job lined up, but due to the recession, the backup fell through, and my business struggled. It made for a very tough few years even though I had avoided buying a house during the peak of the housing boom and instead bought one near the bottom in late 2008. If I had understood more about economic cycles at the time I would have waited a year or two before leaving my stable job.

Alright, there are obviously more things a person can do, and each person’s situation is different, but at least I hopefully conveyed the spirit of what I’m getting at. This is not a time to be making big purchases, taking on extra debt, or making a risky career move for most people.

And, one last note. Even if you appear to be in good financial shape yourself, there are many knock-on effects when demand for goods and credit dry up during recessions. Just because you aren’t highly levered personally, doesn’t mean the customers of the business you work for aren’t. The reduction of available credit, which is what the Fed is trying to do by raising interest rates, reaches farther than many people understand in the economy. The economy runs on credit and we are all interconnected much more closely than most people realize. So, you might be behaving in a very prudent way with your personal finances, but that doesn’t mean the business you work for is, or the customers of the business you work for are. Because of this, in order to be safe, we almost always have to be more prudent than we instinctively think we do during a recession. My suggestion is to try to make some of these adjustments sooner, while times are still good, rather than later.

Now, I am not Dave Ramsey or anyone’s financial advisor, and these aren’t things that I typically write about or even feel comfortable writing much about. But, they are very relevant to investing. The reason for that is when we have a dip in the short-term debt cycle that causes a recession, you are not going to be in a position to have the cash and confidence available to take advantage of the corresponding dip in the stock market if your personal finances are not positioned to do so. Stock markets don’t just magically get cheap. When they get really cheap, it’s because people do not have the cash or courage to invest. And if you are worried about paying your mortgage or your car payment, or you have just watched your retirement fund drop by -50%, you probably aren’t going to be in a position to be a buyer of stocks at that point in time.

There is a scene in the movie “The Empire Strikes Back” when Luke Skywalker is training with Yoda and decides it’s time to face Darth Vader in order to save his friends. Luke tells Yoda that he is “not afraid”. And Yoda responds in a very dark and ominous voice, uncharacteristic of his behavior up to that point: “You will be. You will be.” I feel a lot like Yoda felt about Luke whenever I hear someone tell me about how they won’t be afraid to “back up the truck” or buy “hand over fist” when stocks get really cheap. Without proper training and preparation, it’s unlikely to be the case.

How to Prepare For A Bear Market

Alright, now that we all have our personal and professional lives fully prepared for a recession, we can properly focus on how to prepare for a Bear Market. This is going to vary a lot from person to person as well, so I’m simply going to share what I have done and what I am currently doing to prepare for a moderate-to-deep bear market. One of the edges I have as an investor is that my personal finances are pretty conservative and I’m not afraid to invest in stocks during a deep decline. I always have a plan, and while I do make adjustments around the edges, I mostly stick to my plan. I bought on the way down in 2008 until I ran out of cash, and I bought about 30 stocks in March of 2020. So, I know I will keep buying if stocks hit the prices I want, and I’ll keep buying until I run out of money. Not everyone is like that. My audience is investors who want to produce above-average returns in the stock market. Part of the way I do that is by avoiding significant parts of a big downturn, and the other way is by buying quality stocks during a downturn that will have more upside than the market when we come out of the downturn. Let’s focus on the first step because that is closer to where we are in the cycle right now.

First, one of my core rules of investing is that I don’t buy stocks that I would not be comfortable holding through an unexpected downturn. Even though I often sell stocks when they are expensive or when I think they have a disproportionate likelihood of a big drawdown, I only buy the stocks that, if I am wrong about the start of a bear market or cyclical downturn in an industry, I can always simply hold the stock through the downturn without much worry of bankruptcy or permanent impairment. So, I want stocks where if I get a cycle wrong I still do okay, and if I get it close to right then I do much better than average.

One of the first things I did when it looked like a bear market and recession were getting more likely back in late December and January, was to sell or put trailing stops on the stocks I owned with deep price cyclicality. There are two types of these stocks, the first type is what I call deep cyclical stocks, and these are stocks whose earnings tend to fall by -50% or more during recessions. An example of this type of sale was U.S. Bancorp (USB) which I wrote about back in January in my article “U.S. Bancorp: Why I Recently Took Profits in USB”. Part of the reason I took profits in this deep cyclical was that it had met my return goal of 100%, and the other reason I describe here:

A big change happened this December, however. The US government, led by Senator Joe Manchin, decided that inflation was a problem and that they wanted to withdraw fiscal stimulus from the economy. Combined with that change, the Fed quickly reversed course and decided inflation was a problem as well, and they started decreasing their stimulus of the economy as well. It’s my view that pulling stimulus away so quickly will cause a boom/bust environment for stocks, and that unless the government and central bank change course in the next 3-6 months, they’ll trigger a bear market. Since I don’t want to hold cyclical stocks in a bear market and USB was near its previous high price, I took profits.

So, my first step in preparing for a bear market was to sell most of my deep cyclical stocks. I did make exceptions for two categories of deep cyclicals, though: oil-related stocks (in my case, refiners), and auto-related stocks. These stocks, because of additional waves of COVID and supply-chain issues, still had not recovered from 2020’s downturn. So, I continued to hold these stocks in the hopes that they might be somewhat counter-cyclical and have a chance to recover before an actual recession started. So far, that decision is working out, okay, and in the past two months, I have taken profits in my Valero (VLO) and HF Sinclair (DINO) positions with 100% gains in both of them. I am still holding my Phillips 66 (PSX) position, along with auto-related stocks like BorgWarner (BWA), waiting to see if they will reach their return goals before the next recession as well. Overall, though, I’m looking to sell most non-oil-related deep cyclical stocks because they have deeper downside potential during a bear market.

My next step was to sell deep price cycle stocks. These are stocks whose earnings might not fall too much during recessions, but their stock price has a history of much deeper declines. Stocks like this include names like T. Rowe Price (TROW), which I sold back in January. I simply don’

t want to hold stocks that will likely have deep price drawdowns so most of them I sold, and I only held onto a few like BlackRock (BLK) and Meta (FB), just in case I ended up being wrong about the cycle turning down, or in case policymakers changed their minds. (As it turned out, they appear not to be changing their minds, but these decisions were made back in December and January before there was as much clarity.)

After selling most deep cyclical and deep price cycle stocks, I then turned my attention to what I have termed “boom/bust” stocks. These are stocks that had very good earnings growth years in 2020 and 2021 due to stimulus money. I’ve written about this topic extensively this year, but my first example was the selling of LKQ Corp (LKQ) back in January which I shared in my article “Why I Took Profits in LKQ Corporation”. In late December I went through every stock I track, and marked all the stocks that had this earnings pattern to sell or avoid them. I also wrote a well-read article explaining this pattern about Apple (AAPL) and Alphabet (GOOGL) in February titled “Apple & Alphabet Will Not Side-Step A Deep Bear Market”. If you want to understand the “boom/bust” profile, I suggest reading that article.

Once it was pretty clear a bear market was coming back in late December, basically I started selling my riskiest stocks. But because there was some uncertainty as to what policymakers would do, and there wasn’t any clear sign the market had topped, instead of putting the money from those sales into cash, at the time I was putting the money into a 60/40 proxy ETF (AOR). So, even though I was derisking my portfolio back in January, I wasn’t fully bearish, yet, because the outcome of the bear market was mostly in the hands of four people: President Biden, Jay Powell, Joe Manchin, and Vladimir Putin. If these guys had decided that a bear market and recession wasn’t the outcome they wanted they could have changed course at any moment. But Putin decided to invade Ukraine, and at that moment I decided that a 60/40 proxy like AOR was not defensive enough so I moved that money in late February, to cash. At the time it represented about 15% of my portfolio.

I’m sharing this process because it is very different than what people generally think of as “market timing”. While, because of the circumstances, I had to make a very bold call back in February 2020 that put me 70% in cash at the time, this time around is very different. Basically, as the year progressed and economic and market risks rose, I adjusted accordingly.

Because of the nature of the boom/bust risk I’ve written so much about, I recognized that we were in a situation where leading economic indicators were not going to be useful at predicting a market decline. In my marketplace service, The Cyclical Investor’s Club, until very recently when I started buying some fast-growth stocks, my goal was to get S&P 500 returns or better (I aim for 15-20% annual returns over the long-term) while taking on 60/40-type risk. This means that usually during downturns I am much more defensively positioned than the S&P 500. However, I also (with the very brief exception of January and February of this year with AOR) do not own long-term bonds because they were crazy overvalued. So, instead, I held a variety of international stocks like utilities and telecoms and ETFs, as well as metals ETFs, as a way to diversify away from the US market because the US market was pretty expensive, too.

My last portfolio adjustment that involved selling in order to position more defensively had to do with these stocks in the portfolio. Because we could not rely on economic indicators (though I did keep a close eye on 30-year mortgage rates and whether they were over 5% or not) I relied on a simple technical indicator on whether the S&P 500 was trading above the monthly simple moving average or not. When the S&P 500 fell below that level, then I fully went into what I call “Bear Market Mode”, slightly different than the “Recession Mode” from 2020. This occurred at the end of April, and on May 2nd, I sold all of my bond alternatives and put them into cash. When this was all said and done, I was about 1/3 cash at the beginning of May, and that’s still where I’m at.

This entire, relatively slow, process during the first four months of the year has caused my portfolio to fall at about half the rate of the S&P 500 so far, and now I think I’m fully positioned for a moderate bear market.

So, with regard to selling in preparation for a bear market, I would:

- Sell deep cyclical stocks unless there is reason to believe they will be counter-cyclical because they hadn’t recovered from COVID, yet (like oil and autos)

- Sell stocks that have a history of deep price drawdowns even if they aren’t that cyclical

- Sell stocks that benefited greatly from government stimulus because that stimulus has mostly ended

- Sell long-duration bonds, expensive stocks, and anything not high quality enough to hold through a downturn

- Personally, I would not hold more than 50% cash because there are still a lot of wealthy people (and corporations) with cash on the sidelines, and they might come in as buyers early enough to prevent really great stock prices, especially in popular stocks that are viewed as safe

I’m Still Actively Buying Stocks

Importantly, I didn’t go through this selling process so that I could hide in cash. I did it so I could be prepared to buy quality stocks at very good prices if the opportunity arises. So, even while I was selling 30-40% of my holdings, I was also buying opportunities whenever I found them. I run an unconcentrated portfolio so my typical initial weighting is 1-2% for new positions. Since the beginning of the year, I have purchased 13 positions. Three of those were cyclical oil-related positions since I’ve been selling my refiners and I had no other oil exposure. Seven of the positions were fast-growth stocks that tended to be -50% to -70% or more off their highs (these are exclusive ideas for my marketplace service (and most of these have fallen further since purchasing them)). But there have been three stocks that I purchased using my standard “full-cycle earnings” analysis, and I will share those to give an idea of what I have been buying.

The three stocks I’ve purchased this year that I haven’t written publicly about are Netflix (NFLX), Global Payments (GPN), and Fiserv (FISV). I bought them because I thought the valuations looked attractive based on past performance. Global Payments and Fiserv I bought back in January when I still had some hope we might avoid a bear market and recession, and Netflix I bought just a few weeks ago because I think they will eventually be able to grow earnings double digits again.

The point here is that I am actively looking to buy quality stocks when they hit the prices I want. I have one or two additional factors I include in my process because I think earnings estimates are still too high for most stocks. And I have a slightly different and less conservative process I’ll use once those earnings estimates do eventually come down. But I am not looking at the macro for some sign of a bottom for when to “get back in”. I’m still 2/3rds invested in individual stocks, and 1/3rd cash, and whenever a stock hits the price I’m aiming for I’ll buy it whether it’s tomorrow, or in six months, whether we are in a recession or not. So, other than controlling for what I expect will be disappointing earnings over the next 6-9 months, I’m just using my normal valuation process applied to individual stocks, and my buying process doesn’t have any “timing” to it at this point.

That said, I do have some general expectations about where the best stocks to own over the next three to seven years will come from. My expectation is that because the baby boomer generation was such a large generation and because they are very wealthy compared to younger generations and retiring at record rates, it is unlikely that the stocks these investors generally find attractive will sell at very cheap prices during a downturn. An additional factor that makes me think this way is that these types of stocks are already very expensive in most cases so they would require massive declines in price to become attractive to me.

For example, stocks like Proctor & Gamble (PG), Coca-Cola (KO), PepsiCo (PEP), Waste Management (WM), Clorox (CLX), Hershey (HSY), McCormick (MKC), Hormel (HRL), Apple (AAPL), Costco (COST) and Church & Dwight (CHD), would all need to drop about -40% or more from here before I would get interested in buying them. I doubt that will happen without a deep and extended recession which is not currently my base case. There are simply too many wealthy retirees that would step in and buy them at higher prices than I am willing to pay.

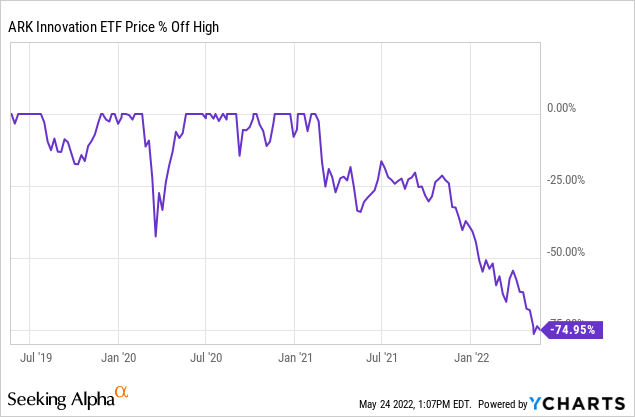

Because of this, I expect most of the best long-term opportunities to come from growth businesses that get tossed out with all of the 1,000+ IPOs and SPACs that came public over the past three to four years. Somewhere in that wreckage of stocks that are down -80% off their highs, will be a dozen or two dozen businesses that will produce great returns over the next decade, so I’m focusing a lot of my attention on that group of stocks even though I know I probably won’t buy near the bottom and that they will be very volatile. The reason I think this will happen is that the investor base that initially invested in these stocks, will have mostly been wiped out by the time this is all said and done, and retirees are less likely to look toward these types of stocks while in retirement and after they just watched them get crushed to nearly zero.

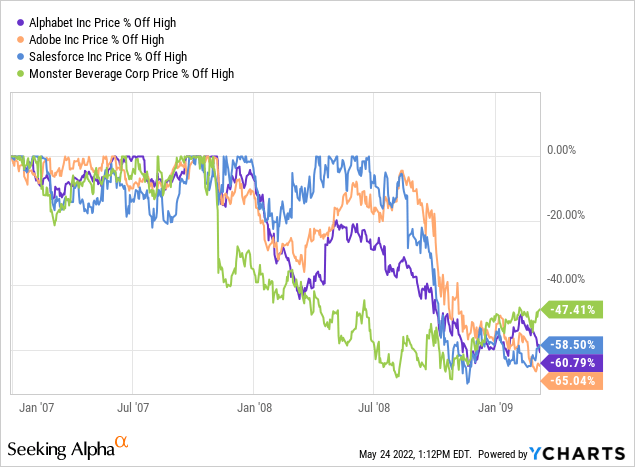

ARKK Innovations ETF (ARKK) is now down -75% off its high, and I don’t think we are likely done, yet. This is the sort of carnage I think the best future opportunities will arise from, but sorting through it is going to be hard, and the volatility, even for the winners, will be huge. But, that is what we saw during the 2008 recession for some of this past cycle’s biggest winners.

Alphabet (GOOGL), Adobe (ADBE), Salesforce (CRM), and Monster Beverage (MNST), all saw huge gains over the past 12 years, but all were down -60% to -75% during the 2008/9 bear market.

If we do end up in some sort of extended stagflationary environment, while many investors will hide in commodities and real estate, I actually think the best defense is going to be earnings growth. Inflation of 5% doesn’t matter as much if you can grow earnings at 15% or 20%. So, broadly speaking, these are where I expect the very best deals to be during the coming downcycle (even though I will buy deals wherever I happen to find them).

My general tips for buying into a bear market like this one are:

- Be patient and give earnings expectations time to come down. I expect negative earnings growth for many stocks, so valuation estimates need to take that into account until we get into 2023 when earnings expectations are more realistic.

- Buy stocks whenever long-term returns from earnings look attractive using conservative estimates. Don’t wait for the macro to change.

- Pay special attention to fast-growing businesses that are profitable, and trading well off their highs.

- Don’t go all-or-nothing. Keep holding quality stocks that aren’t overly economically sensitive, and still trading at reasonable valuations. Personally, I think less than 25% cash is probably too little, and more than 50% cash is probably too much for most investors who are looking to buy individual stocks in an unconcentrated portfolio, but that’s just a rough guide.

Conclusion

Investing during bear markets and recessions is very difficult. In order to achieve above-average returns, investors have to insulate their investing from personal finance dangers as much as they can. It also helps to get defensive in one’s portfolio before the bulk of the bear market occurs. This involves selling overvalued and deeply cyclical stocks in favor of more defensive ones or cash.

It also involves not buying back in too soon before earnings expectations have come down. This is roughly where we are right now, when it is after earnings or earnings guidance disappointments that most stocks are suffering the deepest declines. My view is that this process has just started, and it will probably take another two or three quarters for earnings growth expectations to become more realistic in a post-stimulus and high fuel inflation world. Valuations can look good for a while, only to have the “E” part of the P/E decline significantly. Investors who buy before the earnings finish dropping will be in for a rough ride.

Generally speaking, I think investments that appear “safe”, like long-duration bonds and slow-growth dividend stocks, will cost investors a lot in terms of lost real returns over the medium term. In short, there will be a very high price to pay for the promise of low volatility and higher dividend yields. While I never found these investments particularly attractive, if inflation continues to run high, the opportunity cost investors suffer in order to lower volatility and raise income yields is likely to be higher than ever.

In contrast to that, I expect the eventual rewards for investors who can identify the highest quality growth stocks over the next 6-12 months, to be very good, especially if inflation continues to run hotter than normal. Though it will be difficult both to find the best growth stocks for the long term and also difficult to hold them through the volatility.

Importantly, I will take whatever the market gives me over the coming months and quarters. So, if I see an old-school dividend aristocrat on sale at the price I want, I’ll be a buyer. It’s just that if I was one of the many investors who limit themselves to that particular universe of stocks, I wouldn’t be sitting on piles of cash, waiting for these types of stocks to get super cheap before buying, because I think the odds on that happening are relatively low. (And if they do, the economy will likely have gotten considerably worse than I currently expect it to.)

My hope is that readers at least find some food for thought in this broad overview of the current market and how I think about bear markets and recessions in practice. I prefer to write about individual stocks, but sometimes it’s useful to zoom out and share a wider view, particularly when the markets appear to be at an inflection point of sorts this past month. I hope you found it useful.