Sakkawokkie/iStock Editorial via Getty Images

It hasn’t been a storybook year for The Walt Disney Company (NYSE:DIS) with shares down by more than 25%. Much of this weakness follows the broader market selloff along with concerns over the company’s digital strategy amid signs the momentum in streaming services is slowing.

The company has also been caught up in some controversy, deeming legislation passed in Florida as discriminatory. In turn, Florida has responded by moving to revoke some special privileges Disney has enjoyed in the state for 55 years. While the actual near-term financial impact on the company is limited, the development has likely added volatility to the stock.

Indeed, there are many moving parts but to DIS our take is that the focus should be on what remains solid fundamentals. Indications are that business is booming at the flagship parks and resorts segment still benefiting from pent-up demand as a post-pandemic dynamic. Theatrical releases for the studio group have also returned with several potential blockbusters on tap this year set to drive earnings higher. We are bullish on the stock viewing the recent selloff as simply overdone, leaving shares looking very attractive at the current level.

Disney’s Political Controversy

Since the start of the year, the state of Florida has moved forward with its “Parental Rights in Education Bill”, which aims to prohibit classroom instruction on sexual orientation or gender identity by teachers for children in kindergarten through 3rd-grade grades. This legislation has been informally referred to as the “Don’t Say Gay Bill” because opponents see it as violating free speech and equal protection rights for the LGBTQ community.

The controversy as it relates to Disney has a few layers. First, employees against the bill are disappointed at the company’s initial muted response impacting the workers in the state. Disney CEO Bob Chapek ended up releasing a letter taking a more direct stance against the legislation and promising to do more to protect company values. When the bill was formally signed into law in late March, Disney issued another press release explaining its goal as a company is for the law to be ultimately repealed by the legislature or struck down in the courts.

The series of events ended up opening up a can of worms for Disney as proponents of the bill and the political supporters of Florida Governor Ron DeSantis viewed the company as overreaching into politics and taking a side on an ideological issue.

As a retaliation, DeSantis moved to repeal an act from 1967 which established the area surrounding Walt Disney World as an autonomous zone, noting other theme park operators in the region do not have the same “special privilege”. While there are some questions related to tax implications, the biggest impact on Disney World for practical purposes are logistical issues like requiring building permits from the city that will need to be sorted out.

Our take is that beyond the headlines, the entire ordeal is overblown. This is the type of controversy that plays out more on social media platforms and cable news networks while the average Disney Parks visitor likely doesn’t care. All indications are that the core theme parks of Walt Disney World in Florida continue to buzz. People are not canceling trips or avoiding Disney services because of the issue.

A quick check of the current reservation schedule shows that Disney World Parks sells out nearly every day. If you want to visit this Friday, April 29th for example, the only option still left is “Epcot”. Several specialized publications have noted that the parks sell out consistently, with last-minute guests simply left out. In other words, it’s business as usual, and any impact the controversy may have had on the stock price is temporary in our opinion.

source: Disney World

DIS Key Metrics

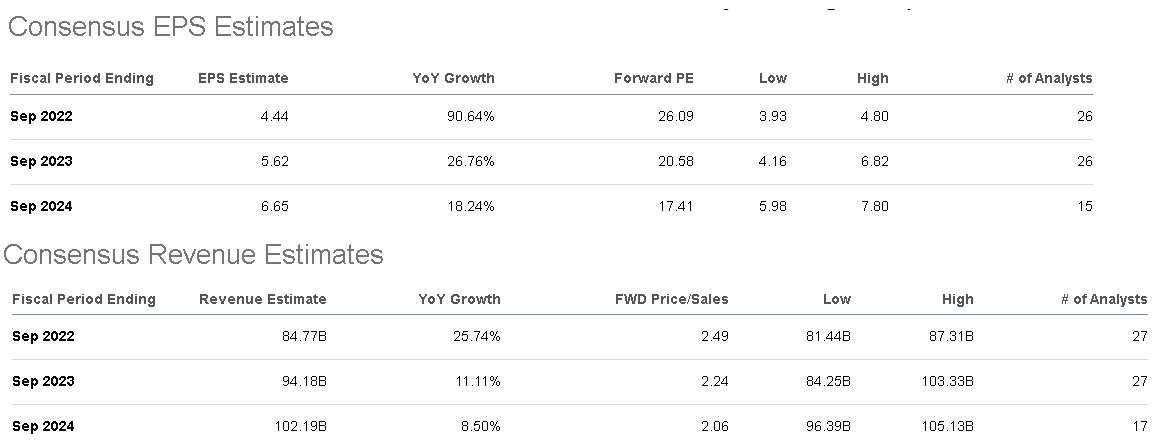

The most bullish sign we see for Disney is its earnings growth momentum. The company is expected to reach EPS of $4.44 this year, up 91% over fiscal 2021, with the pace continuing to average 22% between 2023 and 2024. In our view, these estimates can prove to be too conservative with Disney well-positioned to outperform on the top line in what we see as a positive operating environment.

Seeking Alpha

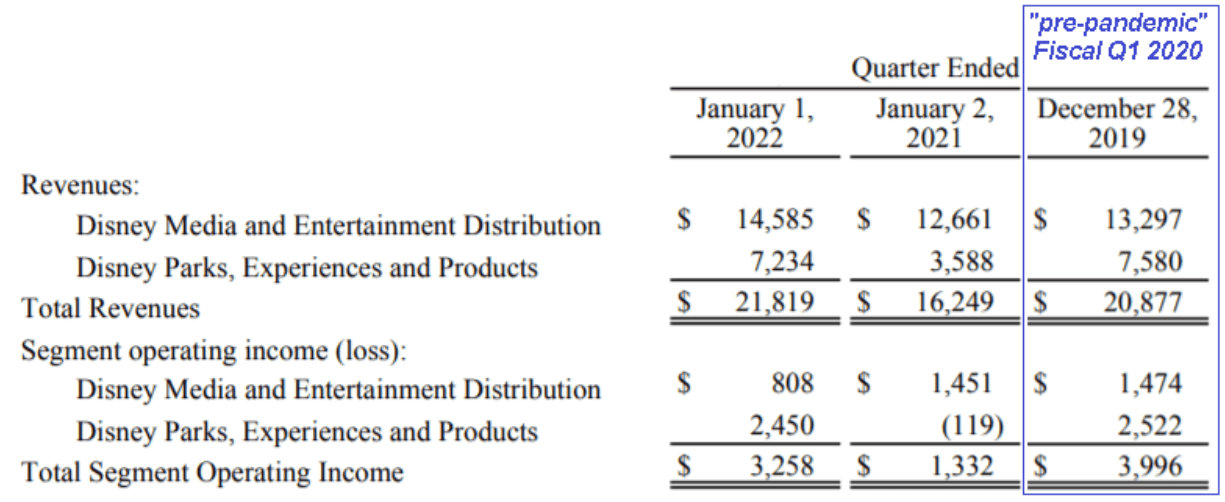

Going back to the fiscal Q1 2022 quarterly report covering the period through January 1st, the big takeaway was that total revenues surpassed pre-pandemic levels. The “Parks, Experiences, and Products” segment stood out with an operating income of $2.45 billion, just 3% below the 2019 record. This is particularly impressive considering the last quarter was defined by the ongoing pandemic disruption including the Omicron-variant surge in December, managed capacity at its parks, mask mandates, and even some resorts not yet fully reopened. The runway is for stronger trends into Q2 and beyond.

source: company IR

The magic of Disney is its ability to raise prices at its theme parks while also capturing the industry trend of rising hotel room rates at its resort properties, helping to support higher margins. Initiatives like the “Genie+” and “Lighting Lane” paid add-on features for faster ride access effectively increase the average revenue per park quest and contribute to profitability. The setup here is for the parks business to have a record 2022 into the upcoming summer months.

Furthermore, there are plenty of reasons to be excited about the “Media and Entertainment Distribution” group. “Disney+” added 35 million subscribers over the past year, while “ESPN+” and “Hulu” also delivered positive results. In contrast to Netflix, Inc. (NFLX) which has struggled to maintain subscriber growth momentum, the attraction of Disney+, in particular, is its content library more targeted toward a younger demographic which ends up being stickier with subscribers less likely to drop off.

What we mean by this is that in many households, particularly with children, Disney+ makes more sense as a must-have streaming service considering its lower price point and the arguably more high-profile intellectual properties between “Star Wars”, and “Marvel”, and Disney Classics. The success of originals like “The Mandalorian” and “The Book of Boba Fett” highlight Disney’s ability to leverage its platform.

Separately, the studio business is set to kick into high gear with an intense schedule of big movie releases. Indications are that industry ticket sales are recovering strongly compared to 2021 with room to improve through the summer months compared to 2019 benchmarks. The end of Covid restrictions should be enough to get people back to the theaters. We believe there are a couple of potential mega box office hits this year among upcoming Disney titles including:

- “Doctor Strange in the Multiverse of Madness” – May 6th

- “Lightyear” (Toy-Story character origin story) – June 17th

- “Thor: Love and Thunder” – July 8th

- “Black Panther: Wakanda Forever” – November 11th

- “Avatar 2” – December 16th

DIS Q2 Earnings Preview

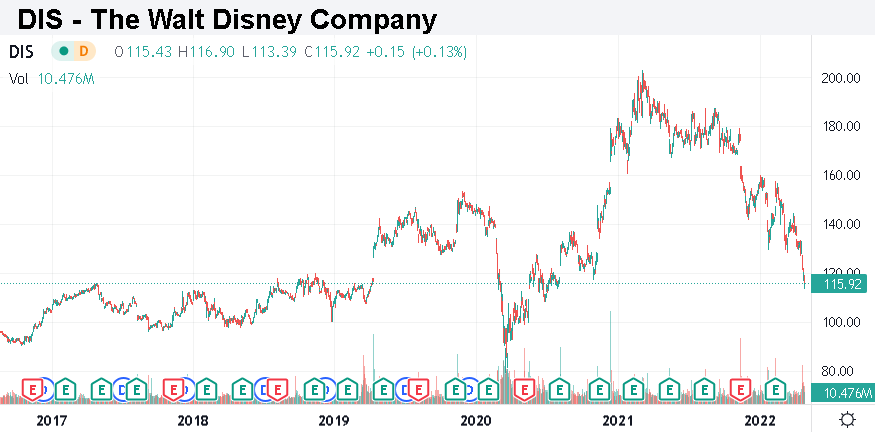

It’s been a brutal selloff for shares of Disney considering it briefly traded above $200 per share early last year and is now down about 45% from its all-time high. The current level of under $120 goes back to a price point for the stock first reached in 2017. A lot has changed for the company over the period including its launch of streaming, but we make the case that the long-term outlook is stronger than ever.

Seeking Alpha

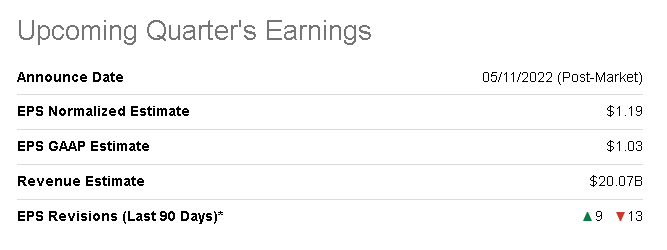

We believe that the upcoming fiscal Q2 earnings release on May 11th could be the catalyst for the stock to reverse higher with more positive sentiment. The current estimate is for revenue of $20.1 billion representing an increase of 29% compared to the period last year. The consensus EPS of $1.19 compares to $0.79 in Q2 fiscal 2021.

Seeking Alpha

If Disney can come out and demonstrate its ability to generate strong profits in the current environment while easing fears of any financial disruptions due to the Florida political imbroglio, the market can shift its focus to what we see as an attractive valuation.

Looking out to fiscal 2023 which covers a full year with a more normalized operating environment, DIS is trading at a 1-year forward P/E of 20.5x. In our view, shares should command a much higher multiple in the context of the earnings growth momentum expected through the next several years. We like the diversification of the business between the parks and resorts cash cow, while the media group has higher long-term growth potential.

Is DIS Stock a Buy, Sell, or Hold?

If it wasn’t clear

enough already, we are very bullish on Disney as a blue-chip leader that is deeply undervalued in our opinion. We rate DIS as a buy with a price target for the year ahead of $170 representing a 1-year forward P/E of 30x on the current consensus fiscal 2023 estimate. Our thinking here is that a series of strong quarterly reports will drive revisions higher to earnings estimates and add momentum to the stock.

Beyond the macro uncertainties and the latest political controversy which, in our opinion, is more or less a nothing-burger, Disney will be just fine. That said, the stock remains exposed to broader financial market volatility and the potential for a deteriorating economic outlook. Weaker than expected trends in consumer spending or lower global growth can represent a headwind for the company. The key monitoring points include streaming subscriber trends across all platforms along the operating margin from the parks, experiences, and products segment.